Lease-Level CRE Acquisition Template

Commercial real estate acquisitions modeled lease-by-lease. Office, retail, industrial, multi-tenant, single-tenant.

A monthly cash-flow model for commercial real estate acquisitions where the lease structure matters. Office, retail, industrial, multi-tenant, single-tenant. Designed for buyers whose IC committee reads every line of the rent roll before they read the returns.

Why This Template

This model is built on lease-level granularity. When reimbursements, recoveries, rollover assumptions, and TI/LC timing drive the deal, modeling tenant by tenant is what holds up. The Lease Overview on the Summary rolls every tenant into a one-page view. The LTV Sensitivity table re-sizes returns across leverage points without a rebuild. City Transfer Tax sits as its own line on the cover page. Things get more layered when several tenants are co-tenancy linked, or when an anchor lease has a kick-out clause tied to the inline GLA falling below a threshold.

What This Model Does

Start with a rent roll. Define your lease structure and operating assumptions. The model flows everything through:

- Income

- Expenses

- Capital expenditures (TI, LC, building-level CapEx)

- Debt (pref loan, initial loan, refinance, with floating-rate support via the SOFR sheet)

- Investor returns (waterfall with preferred return, tiered promote, configurable GP / LP splits, IRR, MoC, profit)

All in one workbook.

Core Capabilities

Lease-Level Underwriting

In office, retail, and industrial deals, the lease roll drives the outcome. One tenant rolling early can take NOI down with it, and blending tenants into an average rent hides that rollover risk, so the model carries every tenant on its own row.

- Lease start and expiration by tenant

- Rent schedules and contractual growth

- Lease rollover and downtime

- TI and leasing commissions

- New lease vs renewal assumptions

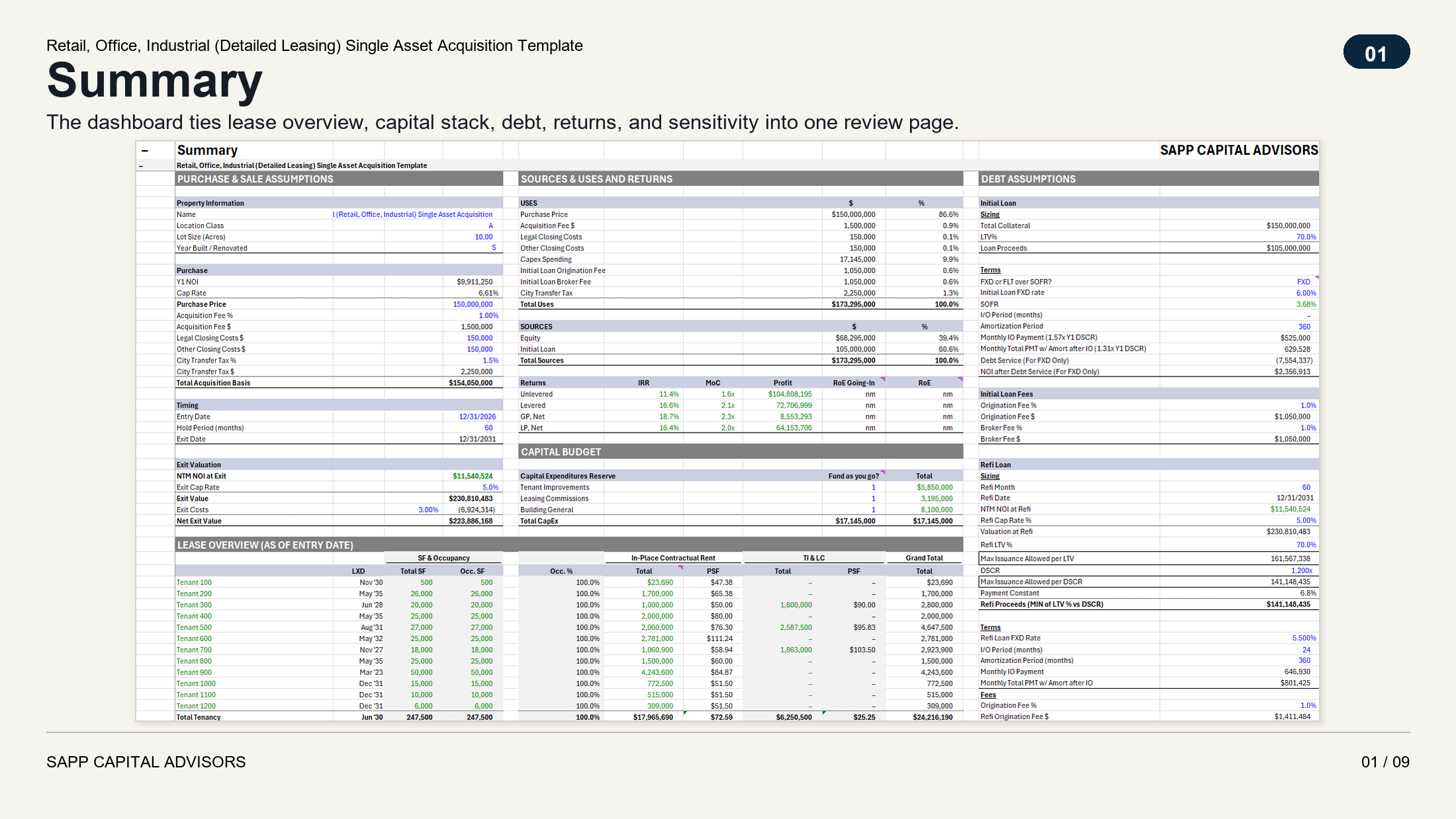

The Summary sheet rolls the rent roll up into a Lease Overview block showing every tenant by LXD, SF, and occupancy, with the weighted-average lease expiration and next rollover risk surfaced at the top.

Flexible Across Commercial Use Types

Designed to work across asset types, not built for one.

- Office, retail, industrial, mixed-tenant commercial portfolios

- Single-tenant or multi-tenant deals

- Scales from simple to detailed lease structures without breaking

Operating Cash Flow Tied to Leasing

Lease activity drives forward-looking property performance.

- Rental income and reimbursements

- Vacancy and downtime assumptions

- Operating expenses and growth

- Stabilized vs in-place performance

Integrated Monthly Cash Flow

Every assumption hits a single monthly model.

- Full Sources and Uses

- Purchase price and closing costs rolled into total basis

- CapEx tied directly to leasing activity

- Debt and equity funding aligned with timing

- Operating cash flow and capital events

- Exit and proceeds

Capital Stack Built for Major-Market Deals

The capital uses section is broken out into Purchase Price, Acquisition Fee, Legal Closing, Other Closing, CapEx Spending, Initial Loan Origination, Initial Loan Broker, and City Transfer Tax. Major-market deals carry city transfer taxes that are easy to leave out until diligence. San Francisco charges 1.5% on the gross. NYC charges 2.625%. DC layers Recordation and Transfer. The deal IRR shifts 50 to 100 bps when the tax line gets back-added during diligence.

Capital Expenditures Tied to Leasing

CapEx is connected to tenant activity, not floated as a separate assumption.

- Tenant Improvements (TI)

- Leasing Commissions (LC)

- Building-level capital expenditures

- Timing keyed to lease events

Debt, Refinance, and Exit

Capital structure options modeled in line.

- Pref loan, initial loan, refinance

- Fixed or floating rate (full SOFR sheet on its own tab for floating-rate deals)

- Interest-only and amortizing

- Refinance sizing on the more conservative of LTV or DSCR

- Exit on forward NOI and cap rate

The Summary carries an LTV Sensitivity table from 0% to 65%, with equity multiple, levered IRR, total uses, and total equity at each LTV point.

Investor Returns and Waterfall

Deal performance translated into investor outcomes.

- Unlevered and levered returns

- GP / LP waterfall

- Preferred return and promote tiers

- IRR, MoC, profit

Built for Audit

Pure Excel. No macros, no VBA, no dynamic-array surprises. Every formula traces back to its source via Excel's precedents and dependents. The IC analyst on the buy-side can audit the model without calling us.

- Global Checks sheet aggregates per-sheet local checks. The model title row shows whether anything is in a broken state.

- Built-in Change Log captures the WHY behind each assumption change, not just the what.

- Color conventions consistent across the library (blue inputs, green cross-sheet links, black formulas).

- Print areas defined on every sheet. US Letter, 0.25-inch margins, repeat rows and columns set.

- An Exit NTM Timing helper on the Summary verifies that the next-twelve-month lookup window stays past the exit date before any refi sizing or exit value uses it.

Print-Ready Dashboard

The Summary sheet is built as an IC-style dashboard. Assumptions, capital structure, returns, and the Lease Overview block all in a presentation-ready layout. Every other sheet prints clean too.

What It's Designed For

- Commercial real estate acquisitions

- Multi-tenant lease-driven assets

- Office, retail, industrial, mixed commercial

- Lease rollover and repositioning strategies

- Analysts and investors underwriting deals in Excel

What It's Not

- Not a back-of-envelope screening model

- Not a development-first model

- Not limited to a single asset type

- Not dependent on macros or complex systems

For cross-template conventions (color coding, check system, change log), see Modeling Standards →.

Use this on your next deal